There are not many places in this country where you can legally turn less than $20,000 into a Million dollars, completely passively and tax-free. Yes, you read that right! Passive income that you don’t even have to pay taxes on? What?! Do you know where you can do this?

The easy answer is your 401K or IRA! Yep.

Let me start by explaining a little bit of terminology.

Then I will explain how you can easily become a millionaire by retirement!

IRA – Individual Retirement Account – an investment account that you gain significant amounts of tax breaks for saving your money in it. You must commit to leaving your money in it until you are older than 59 ½ years old, but the tax breaks are significant, and you will see a great deal of growth on every dollar due to the time commitment. You can break the commitment and pull your money out early, but you will face tax penalties and they can be very large depending on your household income and the amount of the withdrawal.

401K – An IRA that is sponsored by your employer. This is important to differentiate because you have greater savings power through your 401K than you do through an IRA at an outside entity (a bank or company other than the one your employer chooses).

TSP – Thrift Savings Plan – This is the Military Members’ and GS Civilian’s 401K. I must include this because I work every day with Service Members. This is the IRA that has the lowest fees in the nation! TSP is a great cheap option for investing if you have access to use it. You can ONLY invest in it, if and only if you have a paycheck coming in from the government (a paycheck for current work, this does not include military or government civilian retirement, disability, or social security.)

SIMPLE IRA, SEP IRA, and 403b – Other types of IRA they all have various tax laws governing them, but various employers may offer one over the other. They all are investments that are limited by withdrawal after age 59 ½ to avoid penalty.

Let me share a story with you…

There is a 21-year-old woman, she is just starting out in her career. She understands the value of saving money and takes it seriously. She keeps her expenses low so she can save $250 a month in her 401K. We will assume a 10% rate of return, which is a possible average in our stock market over time. She saves this way for 6 years. She has saved $3000 a year for six years which equals $18,000. She never puts another dime in that account. She may have switched jobs and started a different account or had a baby and didn’t have the money to save anymore. Whatever the reason, she stopped at $18,000 invested by age 26. If she just lets that sit and grow at that 10% rate of return until she is 65, how much will she have to withdraw in that account? What do you think? Take a wild guess…

Do you think $100,000? $300,000? More or less?

Well, guess what? That measly $18,000 of hers turned into over a million dollars! Yes, you read that right. It will be grown to $1,047,000! Where else can you legally turn $18,000 into over a million dollars? Maybe in Vegas, but there will be a lot more risk involved with attempting that!

So, what happens if, at age 21, you think you don’t have the money to save or you delay because you would rather “live life” and not think about retirement yet. Let’s say you wait 10 years. Now you are 31 years old. You save at the same rate and timeframe as the first woman. However, you are 10 years later. You save $18,000 by the time you are 36 and then you stop putting into that account. We are assuming it is the same account with the same rates of return. How much will you have to pull out of your account at age 65?

$700,000? $500,000? More or less?

Less! You will only have just over $400,000 in your retirement account! Well, when you think about it, $18,000 grown to $400,000 is still darn good growth! However, what did you lose that the first girl got? You lost $600,000 in interest alone! You lost $600,000 just because you waited 10 years to start investing in your IRA.

The moral of my story is … invest now and invest as much as you can for retirement! There is no time to delay. Time is the magic element with investing and when we are investing for the long term as we do in our IRA, that is when we can see real growth from our money.

I believe it is important to always be investing for retirement. I think everyone who is not in retirement needs to be saving for retirement.

It is easy to give every excuse in the book.

I will save when I make more.

I will save when I am older, I have plenty of time to think about retirement.

I am too young.

I have too much debt.

I think it is too important to wait. When you are using a percentage based spend plan, the goal is to get to the point where you are saving at least 10% of your monthly income. Now, you don’t want to save all 10% in your IRA, but I would be sure I was saving at least part of that every month in my retirement account. Even if you start small with $20 a month and make it a habit. The more debt you pay off, the more income you receive, the more emergency savings you have built, then the more you can save for retirement.

Why shouldn’t you put all your savings in your IRA?

It is important to only put in what you are committed to not withdraw until you are over 59 ½ years old. Otherwise, you will have such large tax penalties and you will lose all the growth potential of that money that it is not worth it.

Put anything you wish to spend before that age in a different type of savings account. An IRA should NOT be used to save for a home, car, or other items unless those things are purchased after you are old enough to avoid penalty.

If you are following a percentage-based budget, then a portion of your savings should be dedicated to retirement. Then as you can save more, keep increasing your monthly retirement amount until you hit the yearly maximums, set by the government. ($19,500 for a 401K in 2019)

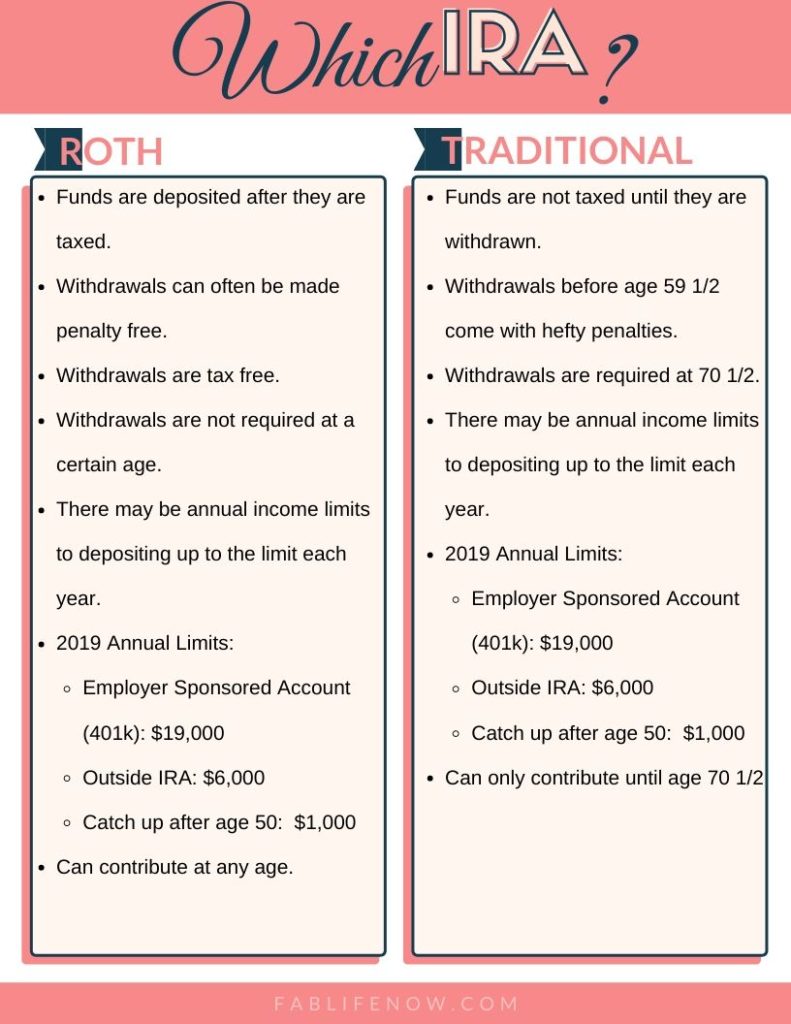

Roth or Traditional IRA?

The easiest way to differentiate these two is simply when you pay taxes on your money. You will always have to pay taxes on your money, that is a given. With an IRA, the government allows a break on your taxes. With Roth, you get the tax break on the growth of the money and with Traditional, you get the tax break on the initial deposit.

In the first paragraph, I mentioned that you could have passive income that you don’t even have to pay taxes on. The growth of income from your initial investments into your IRA can be tax-free IF you choose the Roth option for your deposit. When you choose Roth, you pay taxes on your income before you put anything into your IRA. You will get the tax benefit on the growth of your investment and you won’t owe taxes when you withdraw your funds in retirement.

In my story above, if you choose Roth you will pay taxes on the $18,000 deposited and when you end up with $1Million or $400K you won’t owe another dime of taxes! If you choose Traditional or Tax-Deferred, you will get the tax break on the deposit. Again, in the example above, you would get a tax cut on the $3000 each year that you deposited. However, when you end up with the $1Million or $400K, you would owe taxes on all that money as you withdraw it in retirement.

There is a more detailed answer as to which you might want to choose, but if you evaluate the two options, try to assess which will give you the best tax break and choose that one. I like to simplify it to if you can afford Roth, do Roth. If the tax break today helps you save more today, that may be a good option for you to explore as well. To get a more detailed answer, speak with your CPA or investment advisor as to which is best for you based on your tax situation.

I have created an easy printable to help you distinguish the difference. If you would like to download it, you can find it in my Resource Library. Sign up to get the password to our Library here:

Where do I start an IRA?

- If your employer offers any matching funds on your IRA investments, start there. If you are missing out on their matching funds you are losing out on free money offered to you.

- If you have access to TSP, think of maximizing the use of this option as it has the lowest fees in the nation.

- Look for another low fee mutual fund option. Vanguard and Fidelity are known as carrying some of the lowest fee options. Others that might have some good possibilities could be TD Ameritrade, Merrill Edge, or Charles Schwab.

The easiest thing to do is call the company you are interested in working with and talk with one of the advisors about what you want to accomplish. It is very similar to opening a savings account. They will help you get it set up and then you can start depositing each month or with every check you earn.

I suggest you set up an auto-deposit to put money in your account straight from your paycheck or as an auto-transfer from your checking immediately after you get paid. This will make it more likely that your deposits get into your IRA. If you leave it to the end of the month, often the money you wanted to deposit will have already been spent.

Other posts you might like:

Cutting Costs to Help You Save More

Increase Your Paycheck to Invest More

Don’t forget to Pin and Share!

- Effective Therapists for Counseling Services Near You: Nationwide Referral List - January 18, 2025

- Can You Bring an Inhaler on a Plane? Important Tips - February 5, 2024

- How Can I Hide Money From My Husband Before Our Divorce? - January 21, 2024

Leave a Reply