Let me guess. You opened this article because you have tried several budget sheets and methods, and none seem to work for you.

You would love to know the keys to a better budget, but they seem so elusive.

Some Gurus say to “track every dollar,” and gosh darn it, you have tried! But that is exhausting.

I tried those methods too. I categorized everything by hand and through apps. I have attempted to set budget amounts and then follow them through the month to “stick to my budget.”

Let me be perfectly honest. I am a single mom (period). Enough said.

You could replace that with any of the following.

I am a busy professional.

I own my own business.

I am a stay-at-home mom.

I am a single woman who works hard for my money.

Any of these scenarios leave little time to hassle with the effort it takes to track and categorize every dollar you spend every month or every week.

I have created a solution for everyone. I call it my Simple Financial Success System.

Here are the five steps that I guarantee will immediately help you have a better budget.

Step 1: Stop Trying to Budget Your Money!

Yes, you did read that right. I think the first step to a better budget is to STOP budgeting.

It is time to stop trying to set a limit for 500 budget categories. (I have actually seen pins on Pinterest that share the 500 categories you need in your budget!) Then trying to stick to them all.

Instead, I want you to shift your mindset and habits to create a spending plan.

What is the difference between a spending plan and a budget? You might be asking.

It is partly just the way you name it. However, a budget has a restrictive connotation. One that fun and extras should not be a part of because that is not ‘responsible.’

A spending plan allows you to spend and on whatever you choose.

I recommend you allow enough spending for the necessities like food and shelter before the eyelashes get done, but if you have room for both, then go for it!

Step 2: Keep it Simple

If your plan is complex, it won’t be something you can quickly follow, so you won’t.

You can always add more complexity as you go, but get started as bare-bones and straightforward as possible. When you see yourself following it, and it starts to work for you, you can add more if you want.

The perfect place to start is a percentage-based plan. If you Google or check Pinterest, you will find other percentage-based methods. I’m not too fond of the most popular one, but I won’t take the time to explain why here.

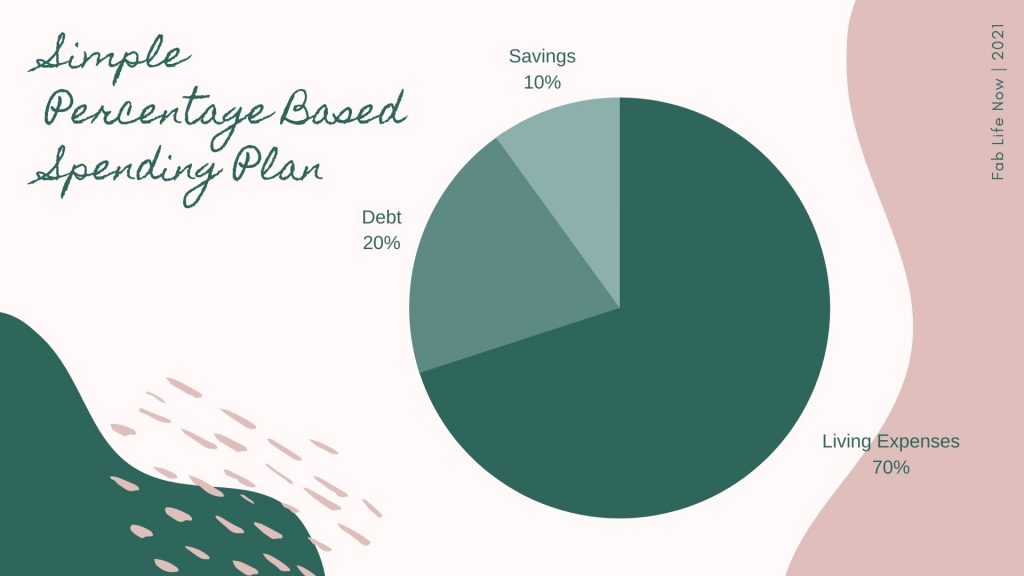

I suggest you calculate your 100% of income for the month. This won’t be hard if you only have one source of income but add all revenue if you have more.

Split that 100% three ways. 70% – 20% – 10% As a place to start or help drive your first goals.

70% or less is your living expenses. This category includes all the money you spend each month on your costs and extras. 70% is a limiting factor for your spending. After subtracting your bills and obligations, you have left over for daily, weekly, and monthly spending.

Using this guideline, decide how much you can spend each paycheck, week, or month. Now you have your spending limit, and that is all you have to track, that you don’t go over that total number.

20% or less for debt repayment. 20% is also a limiting factor. Make sure all the minimum monthly payments for your debts, added together, are kept at 20% or less than your monthly income. If you are not under this, make it your goal to decrease to this.

10% or greater. Aim to save at least 10% of your monthly income. If you have less debt, this can be greater, or if you have lower living expenses, try to save more.

You can save your 10% across multiple accounts like 401K and emergency fund, but try to save at least 10% altogether over the month.

Step 3: Start with your goals

After evaluating where you currently fall on the percentage scale, decide your goals.

Do you need to save more? Do you need to start investing some of your savings? Do you need to reduce debt?

Think in terms of time. Create your savings goals as short (0 to 5 years), medium (5 years to age 60), and long-term goals.

Planning your financial goals with time in mind will help you know where to put your various savings to make the maximum interest you can on each dollar you save.

Step 4: Set it and forget it

Automate as many of your goals or plans as you can.

For example, after you decide to pay an extra $50 a month to reduce one of your credit card debts, set up an auto-payment for it to happen each month.

When you choose to invest an extra $100 in your 401K, set that up to happen automatically through your employer. Set up an emergency fund and other shorter-term savings to come out of your paycheck into a savings account or use an auto-transfer into the appropriate savings account from your checking account.

Set these auto deposits to happen as soon as you get paid, so they happen.

Place reminders on your calendar in your phone for things like payments that vary every month, so you don’t end up with late fees.

Also, use phone reminders for when you do a free trial or a subscription that you don’t want to renew. This way, you won’t end up paying for something you don’t want.

The more you automate, the less you need to think about each month to keep your Spending Plan working for you.

Step 5: Revisit your plan annually or when there are significant changes

Now you have your goals, auto pays, deposits, and spending limits set. You have created a simple system to manage your money.

No more need for spreadsheets, envelopes, or tracking every dollar.

After a few months, you will start to see that your bank accounts are growing and your debts are shrinking with little to no effort on your part!

What a fantastic thing. That is a better budget for sure.

To get more help with creating this new system. I have created a Mini-Course to walk you through it. It is called the Simple Financial Success System, and you can find out more here.

- Effective Therapists for Counseling Services Near You: Nationwide Referral List - January 18, 2025

- Can You Bring an Inhaler on a Plane? Important Tips - February 5, 2024

- How Can I Hide Money From My Husband Before Our Divorce? - January 21, 2024

Leave a Reply