Early on in my adult life, I messed my finances up bad. I can attribute it to two main things.

One, I had little to no financial education up until I was on my own in college.

Two, I had a husband who was determined that debt wasn’t bad so we wracked a lot up to and I just followed along.

I take responsibility for what I did and will be paying on those debts (mainly my student loans that we wracked up for years) for much of my life.

The thing with money problems is, ignorance seems like bliss, but it eventually catches up with you and they are often worse the longer you have ignored them.

After my first divorce, I realized what a financial mess I was in. Well, it is obvious when we are talking collections accounts, wages being garnished, legal debt judgments, and well over $100,000 in student loans for someone in a helping profession! Yikes.

That was when I knew it was time for a change (I wish I figured that out sooner!) and decided to set some financial goals and create a plan of action to start moving forward.

Why should You Set financial goals?

The easiest answer to why it is important to set financial goals is simply that you are more likely to meet financial milestones and move toward financial wellness if you have goals.

Goals are the first step to creating a plan and with a plan, you can start seeing your self get where you want to with your money.

They are the difference between living from paycheck to paycheck during your working life and in poverty as a retiree or having financial stability and freedom throughout your life.

Which would you rather? I would rather live a life of financial freedom!

Print a Goal Sheet to fill in as you work through this.

What makes a smart financial goal?

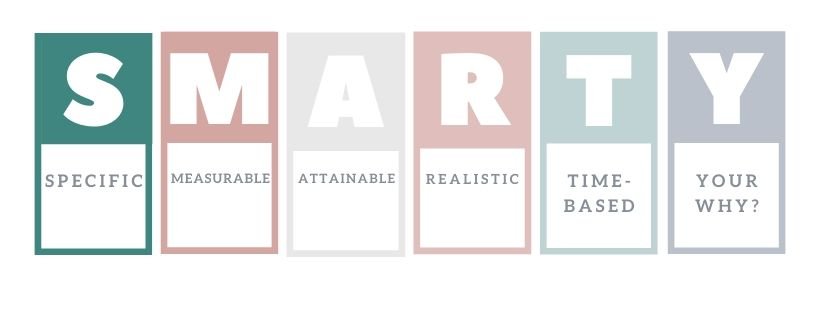

Many of you have heard of SMART goals. If you haven’t, they are

This is a good starting point for financial goals.

When writing any goal, they should be specific, with finances specific usually means quantifiable. Like Save $500 rather than Save more.

Measurable is something you can track. If you are aiming to save $500 you can check your progress with how much your savings is growing toward that final goal amount.

Attainable means that you can attain the goal. A financial goal that would not be attainable for most of us is Save a $1Million in a week.

Realistic means that it is realistic based on your current life situation. It may be attainable for some to save $1000 per month if monthly income is $2000 per month, but is it realistic based on your current living situation? If you have bills that leave it unrealistic, then unless you plan on drastic changes like moving back home with the parents, it may not be realistic for you.

Time – Based means that you put a time frame on your financial goal. I want to save $500 by the end of the year. I want to pay off my high-interest credit card by my birthday. I want to have a down payment for a house by the time I am 27.

These are the basic components of a SMART goal. I think that it is important to take a goal one step further and I have named that system of goal setting SMARTY (you know, like smarty pants? :-b )

The one added component would be to consider your Why. If you add the emotion and motivation to your goal, you are much more likely to stay the course and achieve it, even when the going gets tough.

For example, I want to increase my IRA contributions to $500 a month, by the end of this year. Is a good goal, but let’s add a little more. Because I don’t want my kids’ to need to support me or allow me to live with them in my old age, I want to have enough retirement saved to provide myself housing and health care as long as I live.

That why is such a powerful thing for us mentally. Then we are cutting out our beloved daily Starbucks so we have more to invest in the IRA we can remind ourselves this is so my kids don’t have to care for me.

Why do financial goals need to be time-based?

It is helpful for all goals to be time-based, otherwise, you can work on them forever and never see yourself accomplish the goal.

However, it is even more important with money goals. You need to know when your goal is aiming for. You need to know when you will need the money you are saving for.

Financial goals can be split up between short (under 2 years), medium (2-5 years), and long (over 5 years) term goals.

It is important to know the timeline because that will determine what type of account you save your money in. The longer-term the goal is, the more potential for interest you can gain.

Whether you choose a regular savings account for emergencies, a 3-year CD, a non-IRA brokerage account, or a 401K will all be determined by the length of the savings goal. If you don’t decide how long you can save your money, you may lose a lot of the growing power.

Even if you just keep it all in a savings account with a low rate of interest, you will be losing money.

What are some examples of good financial goals?

Here are some great examples of financial goals.

Save $60,000 for a home down payment in 8 years, to have a home to settle in after leaving the military.

Save $5000 for a trip in 2 years and 4 months, to take my kids to Seattle, where I went to college and up to Canada.

Pay off my two credit cards, a total of $3500 in 15 months by increasing the payment by $80 each month, so I will have an extra $200 to put in my retirement account and have the freedom to travel in retirement.

What are your goals?

Now its time to think through your goals.

Think about what you want to do financially. What is important to you?

To retire early. To pay off debt. To save for a car or a vacation. To begin a nest egg for your children. To save an emergency fund so you can stop living off of credit.

Now, add all the SMARTY pieces to your goal. Make it specific, measurable, attainable, realistic, time-based, and then add your why.

Print out your Free Financial Goal Sheet in the Resource Library. If you don’t have the password, you can get it by signing up here.

Then share some of your goals below in the comments to inspire us all!

- Effective Therapists for Counseling Services Near You: Nationwide Referral List - January 18, 2025

- Can You Bring an Inhaler on a Plane? Important Tips - February 5, 2024

- How Can I Hide Money From My Husband Before Our Divorce? - January 21, 2024

Leave a Reply