I have not always been a good saver. There were times in my life when I viewed saving money as last on my list. For the longest time, I felt I didn’t have enough money to save because I could barely pay for what I needed each month. Then in the seasons where I had enough to pay for the things I needed, I was also purchasing all the things I wanted, as if my money flow would stop tomorrow.

The wise action would have been saving money like my money flow would stop tomorrow. Money has always been inconsistent in my life. Between my two destructive marriages and my unstable life, I haven’t had many years of consistent income where I could build wealth.

I am now 43 years old, is it too late for me to start? NO! I am working on it now. I currently work professionally as a financial counselor and I regularly tell my clients, “Life will happen, and it can tend to derail all our plans. The only thing you can do is look at your financial wellness right now and make wise decisions today and in the future.” It doesn’t help to feel sad or cry over what you should or shouldn’t have done with money in the past. Learn from those things and move forward, one day, one dollar at a time.

I am working to build my savings right now. As a single mom, I don’t have a lot of excess to save. I am, however, working hard to keep my expenses as low as possible and saving what I can. I split my savings between my 401K, my Health Savings Account (HSA), my emergency fund, and my home/travel fund.

My 401K and my HSA are making interest according to the stock market and risk level I chose. There was a time that my emergency fund was sitting stagnant and I wasn’t seeing any growth. Now I am making over 2%. If you are not making at least that, keep reading! If you don’t know how much you are making, it is time to check.

In the last couple of years, the interest rates have been on the rise for loans and purchases. Historically, when loan rates are high, so are savings rates. Some banks, especially most of the big ones are not keeping up with this trend. They are charging us lots of interest to borrow from them, but when we are filling their storehouses with our money, we seem to get nothing in return. I often work with military members, and the top military banks have been resting at 0.1% for savings earnings, as well as many of the other large brick and mortar banks.

When is the last time you checked how much interest your savings account was earning? Have you ever thought of shopping around for a larger rate? Now is the perfect time to do it!

Some of you may be thinking, ‘I have been banking with ABC Bank for years. I like my bank and don’t see a reason to change, not even for 2%.’ That is a perfectly normal response. However, I never said you needed to move all your money and banking to a different institution! Whoever said you need to have only one bank? Many people use multiple banking institutions, using the products at each that has the best deal, rate, or option to suit their needs.

Yes, you can have your bank and earn more interest too! If I was holding more than a couple thousand dollars in my savings at a bank that was giving under 1% interest, I would start to shop around for a new savings account, immediately!

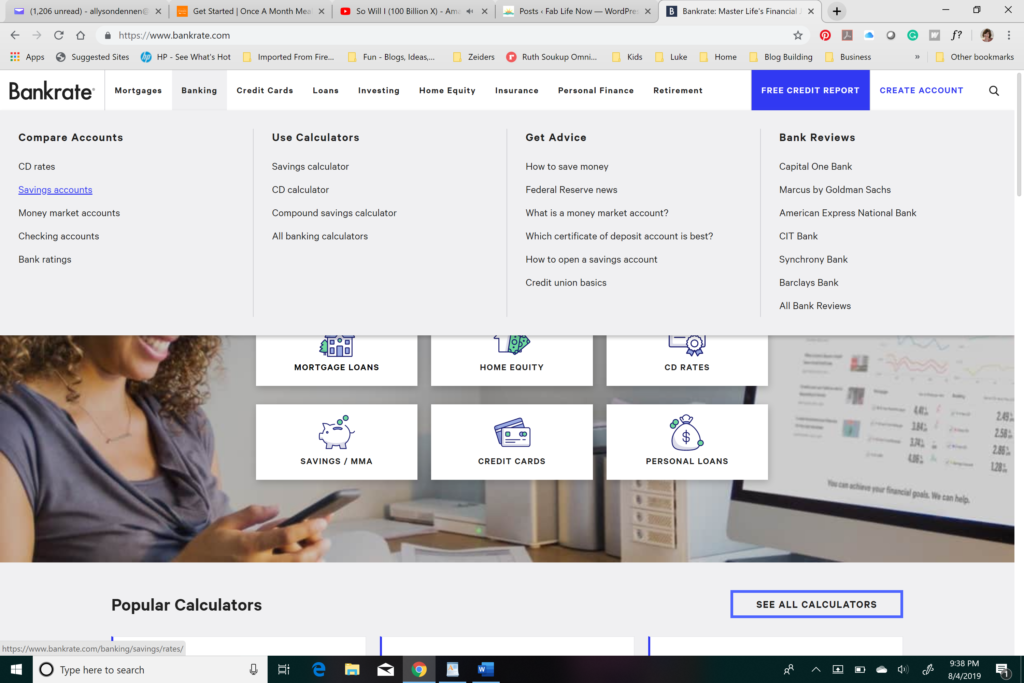

One of my favorite resources for this type of comparison shopping is Bankrate.com. They are a great place to browse for your banking needs. They help you to see what the going rates are for various types of savings accounts and loans and help you choose which will earn you the most interest or pay the least.

When you first go to the website, choose the drop-down menu for Banking. Then choose Savings. Set the search criteria by entering an amount you might want to deposit; you can even just set it as $1 to find the products with little to no requirements for opening an account. Set your zip code, because Bankrate will search for banks that you are eligible to use in your state. On the deposit type drop-down, I like to search for Money Market and Savings accounts and leave the Money Market IRA blank when searching for a savings account. I like to order my search results by APY (Annual Percentage Yield) because let’s face it, I am trying to find the banks that pay me the most!

Once I have my search results, I switch to all products at the top, so it is not filtering out the sponsored banks. Then I have a clear picture of banking products available with the top percentage yields at the top of my list. Start scrolling down the list to see what you can find. What are the top few banks that have the highest percentage currently? This will vary because offers at banks change regularly.

At the time of writing this, the top three are, Popular Direct, Vio Bank, and Salem Five Direct. Have you ever heard of any of these banks? Most of us haven’t as they are either new or very uncommon.

Should you be nervous about putting your savings in a bank you have never heard of? Some of you are shaking your head emphatically yes, right now. How can you be sure it is safe? You want to check that it is an FDIC insured bank. If it is a credit union, you want to make sure it is covered by NCUA. FDIC stands for Federal Deposit Insurance Corporation and NCUA stands for National Credit Union Association. These mean that the deposits into accounts in these institutions are insured for a loss. If anything was to happen to the institution and it was to close its doors, you would be refunded your money due to the insurance. Your money is covered up to $250,000 in each account you have.

Now that you know if the bank you are considering is safe to deposit your money into, the other things you want to asses are ease of use, customer service, and if it can easily transfer to your checking account. The easiest way to do this is to check on the bank’s website for the features you would like. Does it have an app with good ratings? Are there reviews about the bank that you can use to see if customer service is good? I would want a bank with good customer service because if I need my money quickly or call for help with something, I want it to be an easy process.

You may also want to check with your current bank to see if you can link another account to transfer. This way if you want to get your money from your savings bank to your checking or vice versa, you will know if you can do it easily.

You can continue scrolling down the list of possibilities on Bankrate to view more. A lot of credit card companies have high-interest savings accounts these days. Maybe a company you already do business with will offer a savings account that you can use. That would make it easy to open another account.

You can look further into the account and what is offered by clicking the offer details link for each bank on the right side of the list; this will open a window with more details. It will tell if there are fees and if the offer is a limited time offer. I suggest looking for one that is not limited. Limited usually means the high interest will only last for a limited time, then it will drop. Also, watch for monthly fees. Some of the banks will charge one if your account drops below a certain limit, so only choose this bank if you always plan to keep more than their minimum limit in your account.

When you have decided on an account you wish to pursue, you can follow the links on Bankrate to get to the Bank’s website or you can call the institution on your own. Follow the instructions to open the account and then transfer your money.

Now watch your savings grow! Depending on how much you put in, you should start seeing a little bit of interest accumulate each month and boy does that feel good! Be sure to download a Spending Plan Sheet from my Resource Library to help you plan how much you will save and stick to it. Read about why a Spending Plan is better than a Budget to help you move toward your financial goals.

Let us know in the comments below what account you chose or if you found anything interesting in your higher interest rate shopping.

3 Take-Aways

- Many of the big-name banks are not offering more than 0.1% interest on savings accounts.

- If you shop around you can find 2% or more and move your money where it will grow.

- A great place to shop for interest rates is Bankrate.com.

- Effective Therapists for Counseling Services Near You: Nationwide Referral List - January 18, 2025

- Can You Bring an Inhaler on a Plane? Important Tips - February 5, 2024

- How Can I Hide Money From My Husband Before Our Divorce? - January 21, 2024

Informative post! I have a question though. We put our tax return into savings, divide that number by 12 and use that amount to help pay our mortgage throughout the year. Would it still be worth it to move our savings into a higher interest bank even though we will be taking from it monthly? (As long as we don’t go below the minimum amount required to stay in there).

Thanks! Yes, I would move it to higher interest because some of it will be in there all year long. I would also be sure you are not paying a dime of taxes each month. If you haven’t read the post about check it out here. https://fablifenow.com/increase-your-paycheck-without-getting-a-raise/ You should only be getting back child tax credits, be sure you are not overpaying each month so you can pay the mortgage monthly, you will have more control of your money without waiting for the government to return it!